The Token Dollar

The World's Banker Becomes the Factory

I. Kissinger’s Bargain

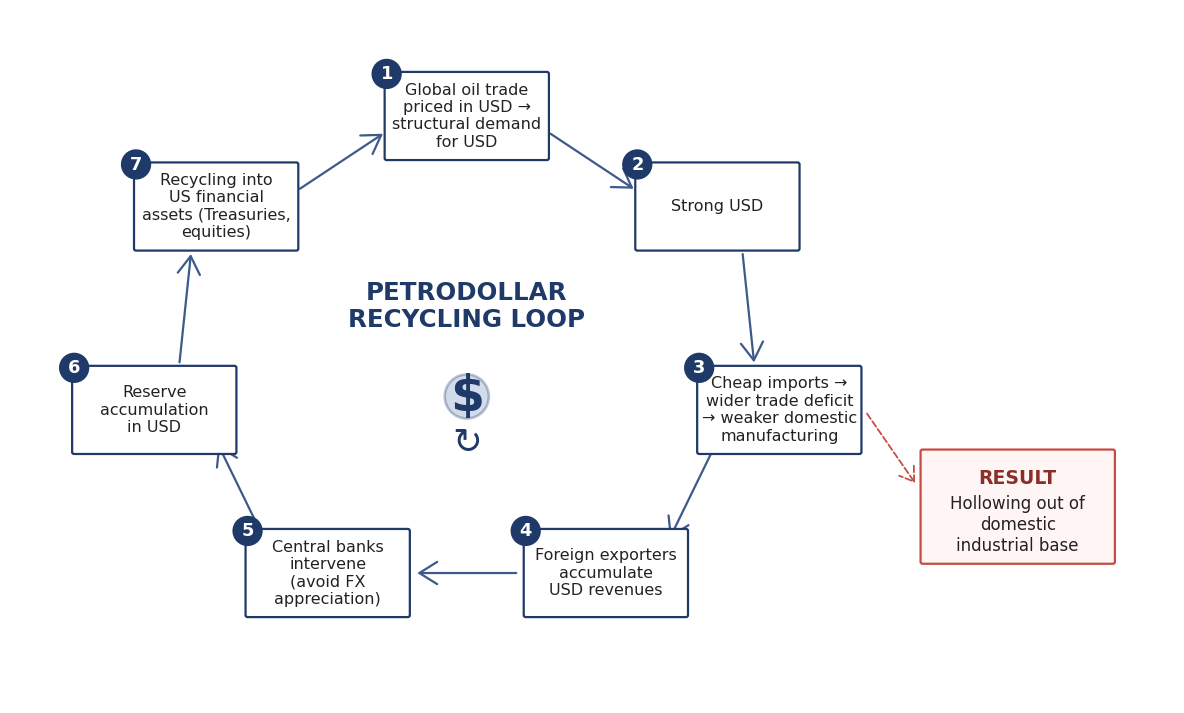

In 1974, in the aftermath of Nixon’s closure of the gold window, Henry Kissinger flew to Riyadh and struck a bargain that would shape the next half-century of global finance. Saudi Arabia would price its oil exclusively in dollars and recycle its surplus earnings into US Treasurys. In exchange, the US would guarantee the security of the Kingdom. The rest of OPEC followed.

The mechanics of this new system were simple and had far reaching implications. Every nation that demanded oil first had to acquire dollars. This in turn strengthened the dollar which made it cheaper for US firms and consumers to import than to produce domestically. At the same time, every dollar earned by oil exporting nations needed to be recycled into the US financial system through the purchase of Treasuries and/or equities. The bargain required it, and the absorptive capacity to spend the surplus domestically simply did not exist. So over time, the dollar became the unit in which the world’s most important commodity was denominated, and the United States became the borrower of last resort, financing its deficits in the very currency the world was structurally compelled and obligated to hold.

This architecture became known as the exorbitant privilege: the world recycled its surpluses back into US financial claims. Foreign savings directly funded American consumption. The persistent trade deficit, which would have been a notable crisis for any other country, became a feature of the system.

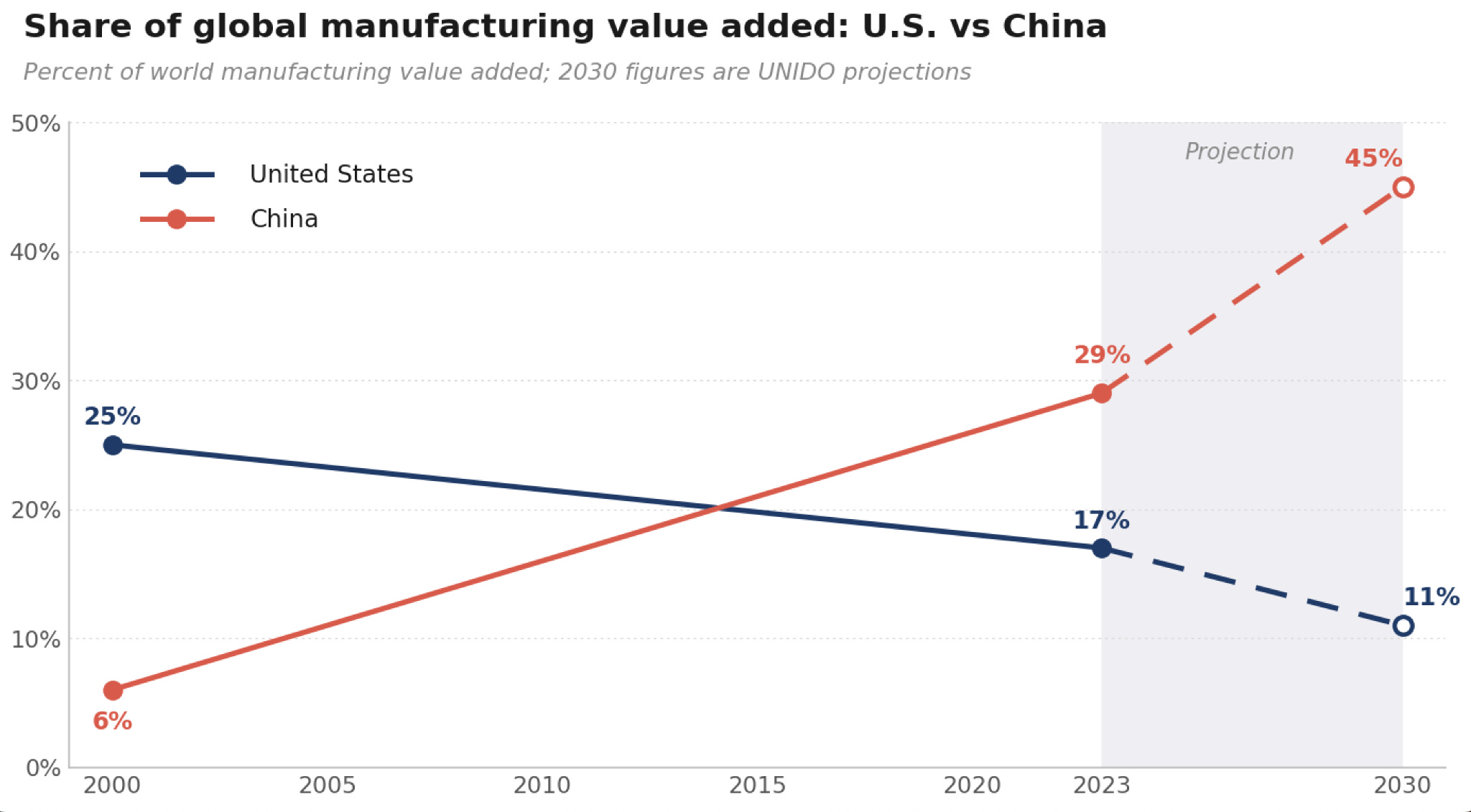

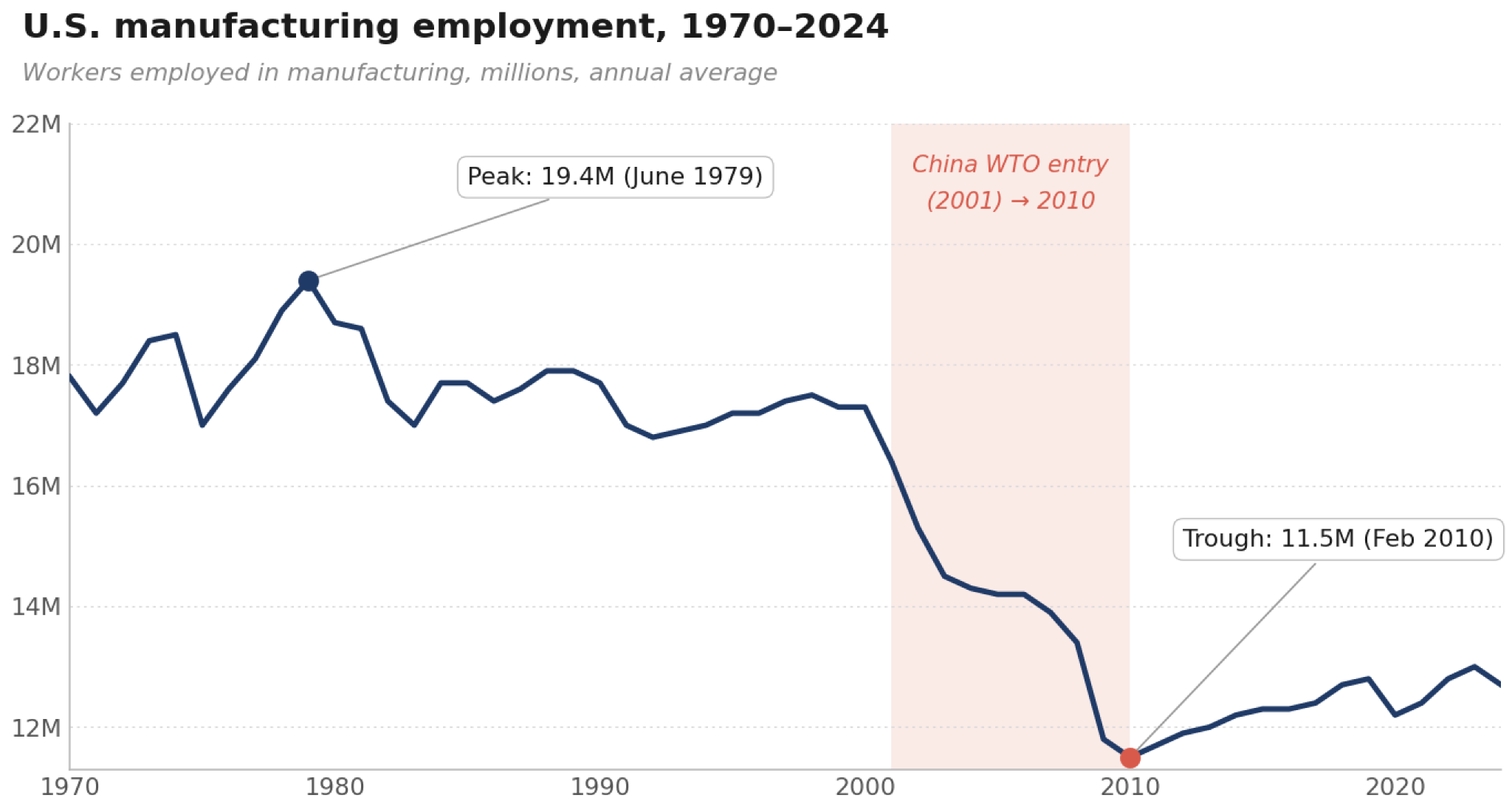

But this architecture did not come without consequences. As foreign capital flooded into US capital markets, the dollar remained structurally strong. And over time, it corroded America’s industrial base. During the span of three decades, US manufacturing employment fell from a 1979 peak of 19.4 million to a 2010 trough of 11.5 million; manufacturing’s share of GDP dropped from 16% to under 10%. China’s share of global manufacturing value added rose from 6% in 2000 to 29% by 2023; UNIDO projects 45% by 2030, against 11% for the United States. To an unknowing observer, it would have appeared that our factories grew wings and migrated abroad.

For four decades, this trade was acceptable. The US got cheap goods, cheap financing, and global hegemony and the world received a stable monetary anchor. After all, there cannot be a solar system without a sun to anchor the orbit of other planets. This architecture became known as the Petrodollar system, and it continues to undergird the global economy. What is changing is the new system being built on top of it.

II. Here Come the Tokens

In datacenters across the United States a new resource is being created on an industrial scale.

Tokens are the output of large language models, and they behave less like a product than like oil. There is no warehouse. Nor a strategic reserve. There isn’t a container ship that carries last quarter’s tokens to a buyer in Frankfurt. Simply put, a GPU spins up, a prompt arrives, an answer streams back, and the thing is consumed in the same instant it was made. Unlike oil however, tokens have one critical property the petrodollar regime didn’t: they are produced by American firms, priced in dollars, and consumed globally.

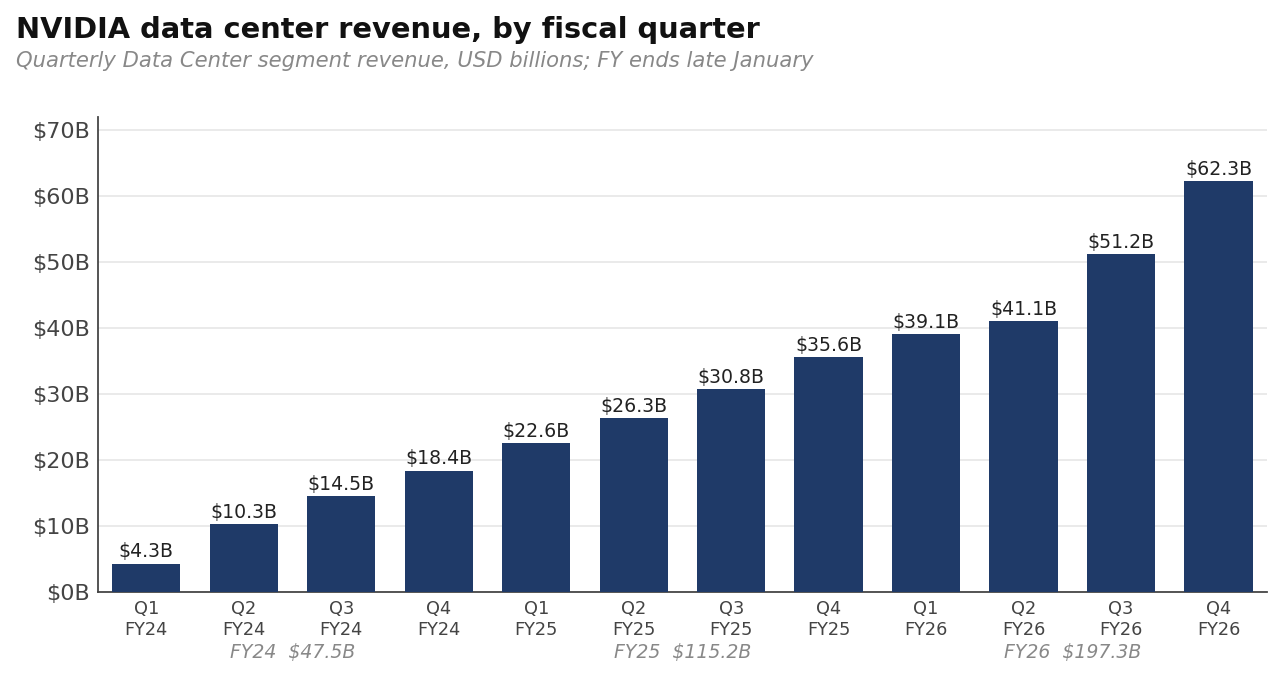

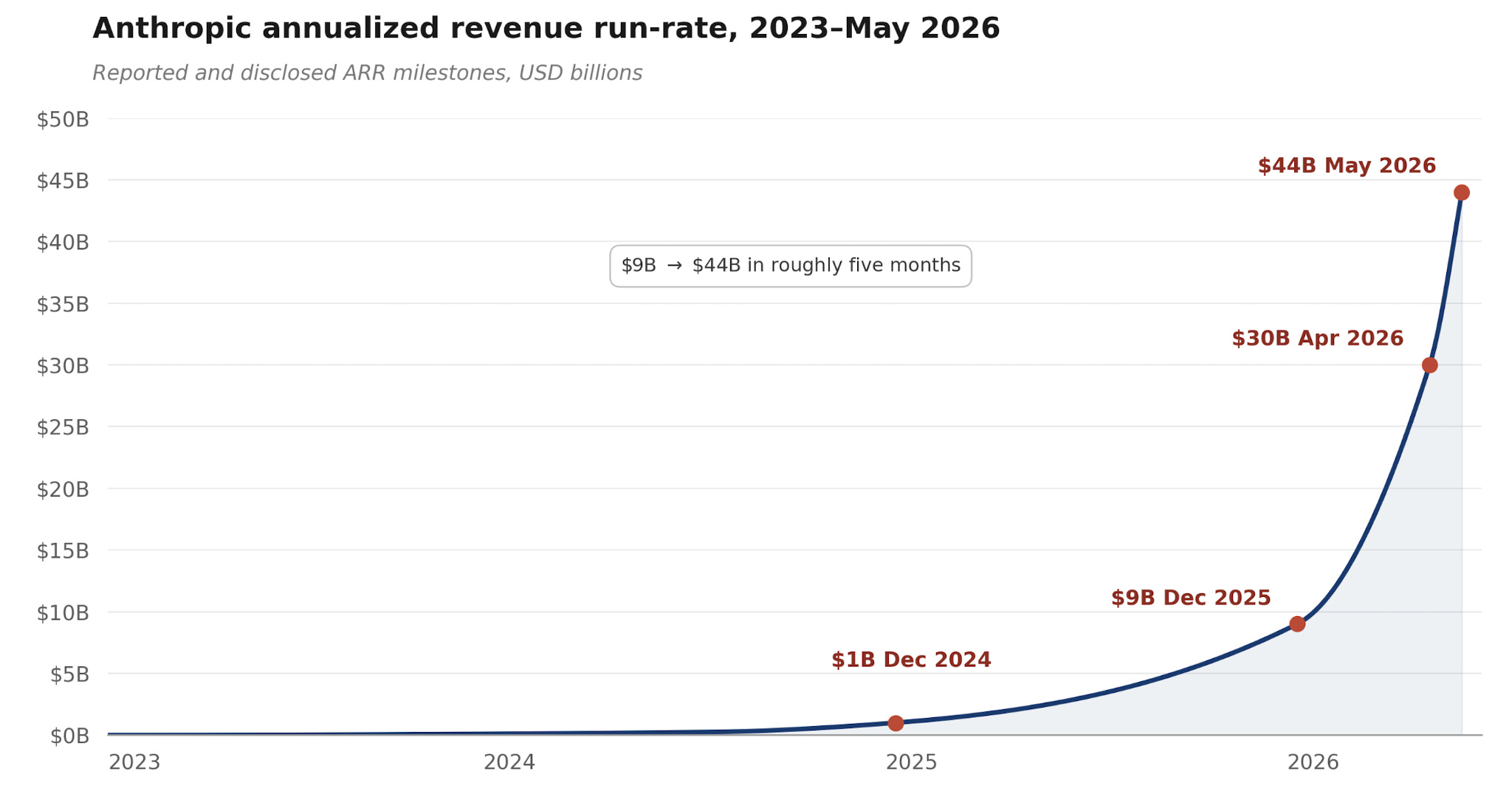

The numbers underneath this commodity are epochal events in the history of capitalism. NVIDIA’s data center revenue ran at $51 billion in Q3 of fiscal 2026 and $62.3 billion in Q4, closing the fiscal year at $197.3 billion in data center revenue alone — up from $115.2 billion the year before. Anthropic’s annualized revenue moved from $1 billion in January 2025 to $9 billion at year-end, then to over $44 billion by May 2026, per SemiAnalysis. OpenAI is on a parallel trajectory. Hyperscaler infrastructure spending climbed from $141 billion in 2023 to roughly $388 billion in 2025, with consensus 2026 projections in the $630–700 billion range. Never before have we seen such rapid growth!

A meaningful share of this demand is foreign enterprises converting local currency into dollars to pay for the commodity that runs the global economy’s cognitive layer. A European manufacturer running inference on Azure converts euros to dollars to do it. An Indian software firm making an API call to Anthropic does the same with rupees. While the mechanics of this transaction vary, sometimes the conversion happens transactionally, with the foreign enterprise paying an American provider directly. Other times, the cloud provider books revenue in dollars and the foreign subsidiary repatriates earnings on settlement. Both arrive at the same end result: foreign currency exits the local economy, dollar-denominated revenue lands on an American balance sheet, and demand for dollars.

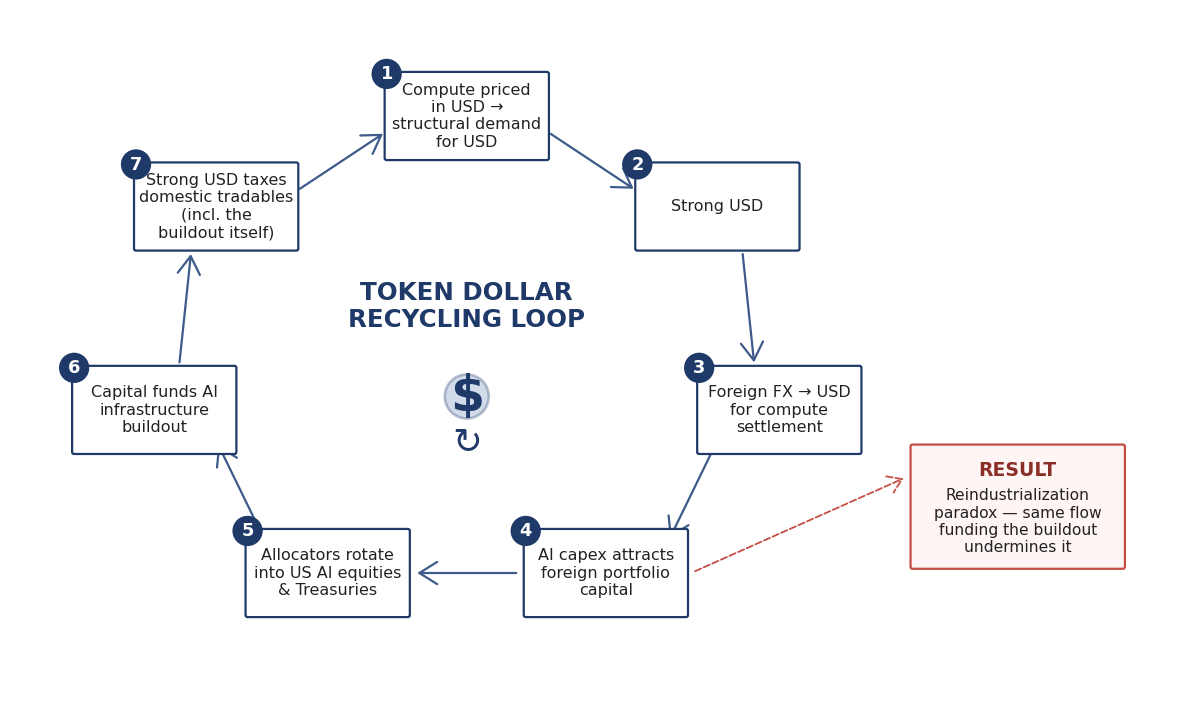

Due to the growth of AI, the United States now produces the two most important commodities of the modern economy — the one that lights the cities and the one that lights the mind— and prices both in dollars. For the first time since Bretton Woods, a single country sits astride the settlement layer of energy and its output simultaneously. The mechanism is being hailed as the Token Dollar. The commodity is compute and the anchor is the American firm that prices it.

III. The Reindustrialization Beneath the Tokens

There is a critical asymmetry between the petrodollar and the token dollar. Oil could be pumped. Tokens must be generated.

To produce tokens at scale, the United States must build the physical substrate beneath them: data centers measured in gigawatts; transmission and generation capacity to power them; advanced fabrication to supply the chips; the long supply chain of transformers, switchgear, cooling systems, optical networking, advanced packaging, and rare materials that constitutes the deep stack of compute. Much of this capacity does not currently exist in the United States. Some of it has not existed in the United States for a generation.

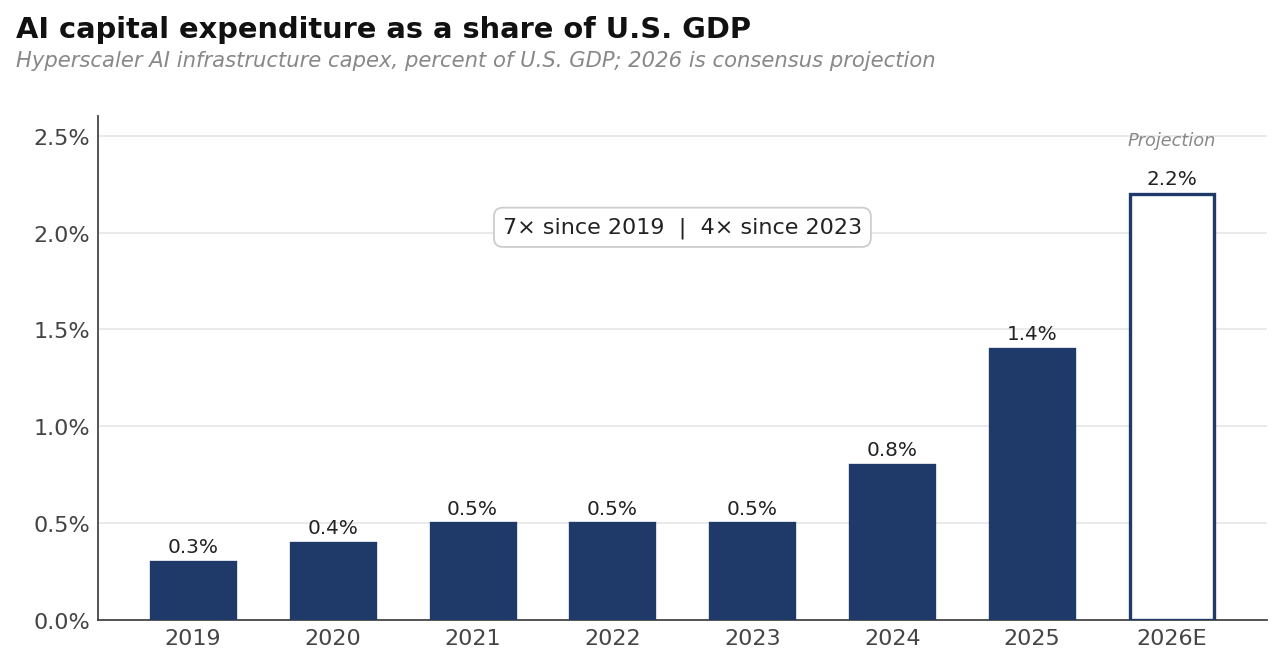

The numbers behind this buildout are staggering. AI capital expenditure has reached roughly 2.2% of US GDP — seven times the 2019 level, four times 2023. Set against historical reference points: World War II mobilization peaked above 40% of GDP, World War I above 20%, the New Deal near 10%, the Reagan defense buildup near 6%, Apollo was just below 1%. Two percent of GDP for a single technology is the largest peacetime industrial investment cycle the United States has attempted since the New Deal and it’s only accelerating from here.

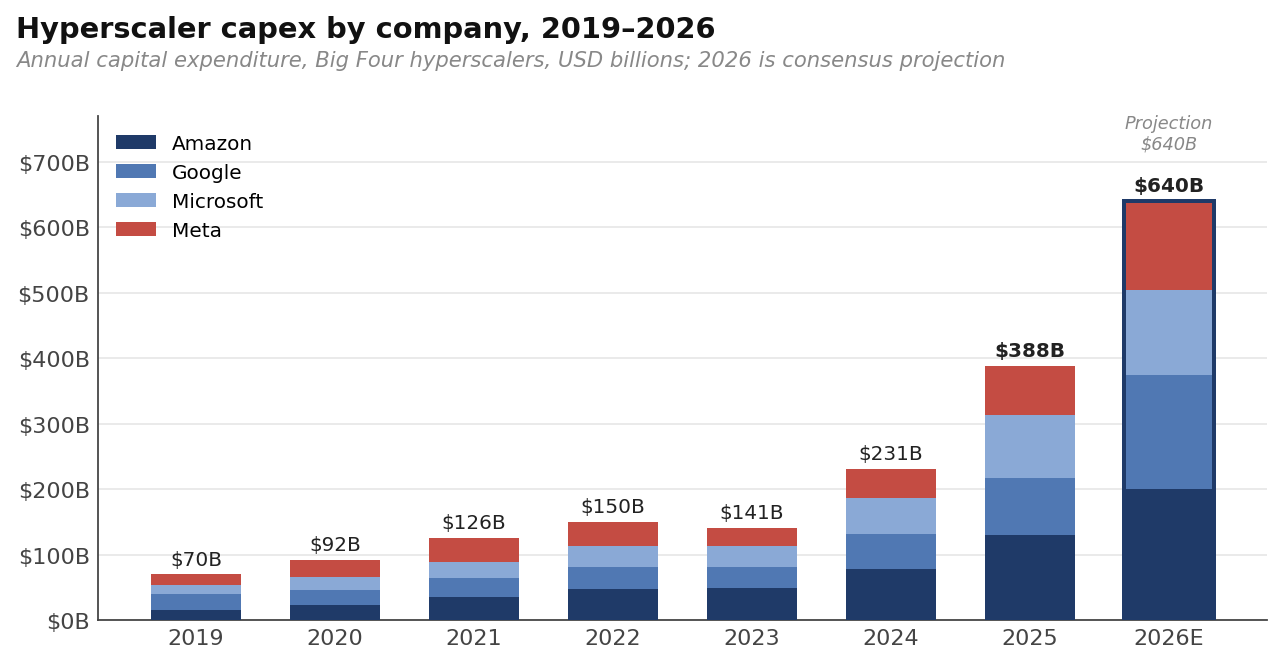

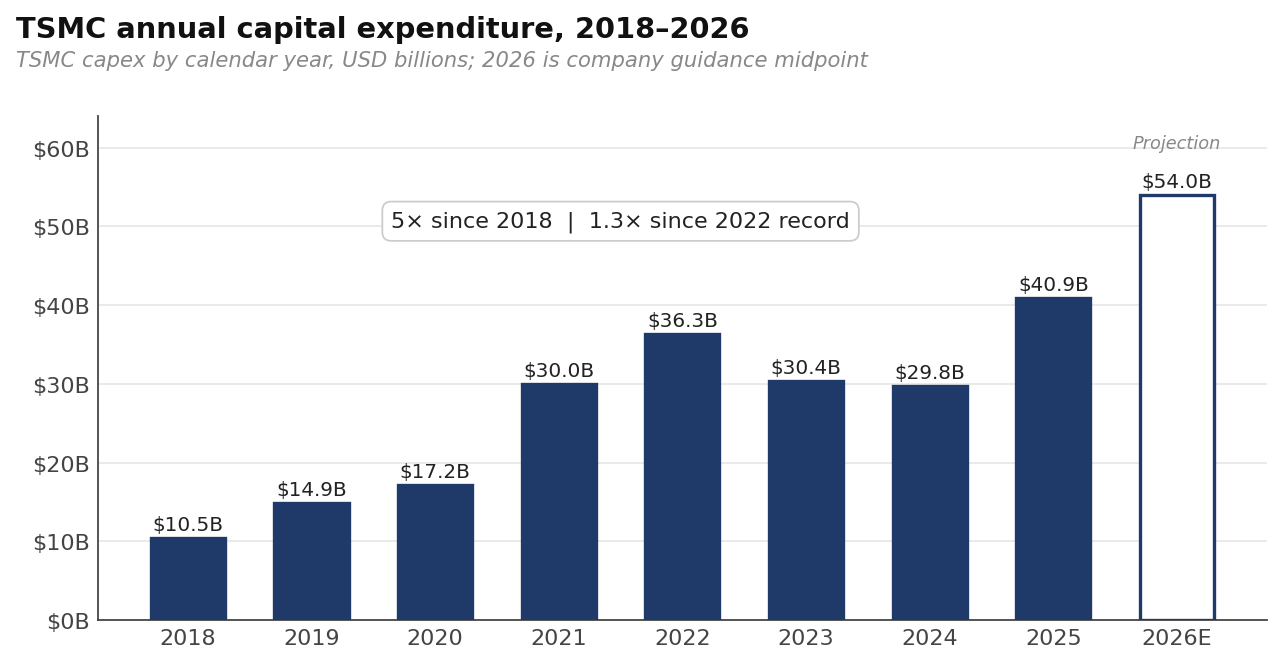

The capital is following the demand at every layer. TSMC has grown its Arizona commitment to $165 billion across six fabs, the largest greenfield foreign direct investment in US history; TSMC’s own 2026 capex guidance is $52–56 billion globally, with three-year guidance topping $150 billion. Hyperscalers issued more than $200 billion in AI-linked credit in 2025 alone, more than double the 2024 total. JPMorgan’s Security and Resiliency Initiative committed up to $1.5 trillion over ten years to critical industries.

David Cahn famously asked in his 2023 and 2024 essays — given all the AI capex, where are the AI revenues? Two years later, the revenues have arrived and are growing exponentially. The Jevons logic is doing the work in real time: as the unit cost of intelligence falls by an order of magnitude, the demand grows. Recently, Dylan Patel, Founder of SemiAnalysis, went onto Invest Like the Best to give his view on the demand to come. SemiAnalysis itself was running a $7 million annual run rate on Claude Code alone against a $25 million salary expense — north of a quarter of payroll with Patel forecasting 100% of payroll by year-end. Elsewhere in tech, Uber’s CTO blew through his entire 2026 AI budget on token costs before the year started. NVIDIA’s vice president of applied deep learning told Axios that spending on tokens now exceeds the cost of his team’s salaries. Tokens and compute are quickly becoming the largest line items on the P&L.

This generational demand spike is being met with a supply side that cannot keep up. Memory capacity currently only grows at low double-digit percentages a year; incremental capacity from today’s demand signal isn’t slated to arrive until 2028. ASML is sold out. Copper foil is sold out. Every lab is supply-limited and sells out of tokens at every price they can charge for them. The economic value the best model can deliver is growing faster than the infrastructure can serve it. All these demand signals and supply constraints are contributing to the topic du jour: The US is Reindustrializing.

IV. Truth and Paradox

“The truth is paradoxical; but man’s passion for rational coherence is even stronger than his love of truth.” ― Aldous Huxley, Proper Studies

While the story being told in headlines is about reindustrialization, the real story is emerging a layer deeper. The same financial mechanism producing the capital that is financing the current buildout will eventually make what funds most of what it funds structurally unprofitable. To state it clearly, the Token Dollar mechanism is working against the reindustrialization it is supposed to anchor.

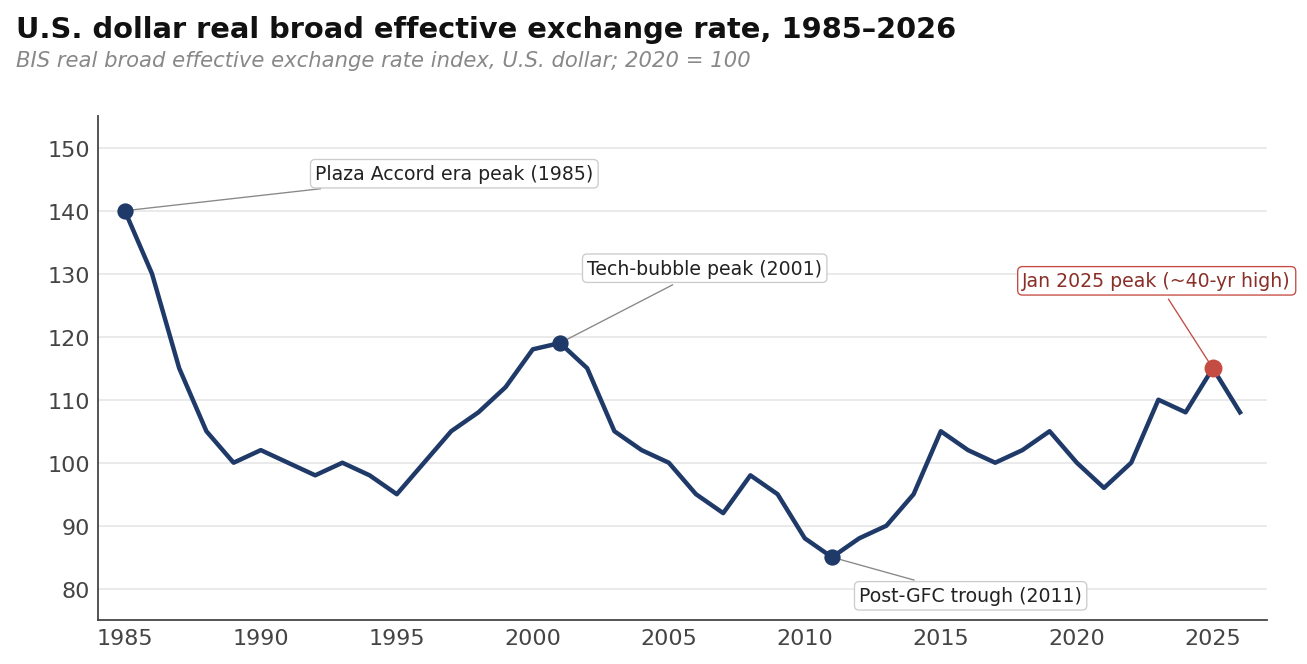

The mechanism is the same one Kissinger set in motion in 1974. Foreign capital flows in and the dollar stays bid, while American tradeables lose on price. What has changed is the scale. The Token Dollar is about to exist on a mechanism with an order of magnitude more capital than oil ever did. Every dollar of AI capex pulls in foreign portfolio capital chasing yield, while every dollar of global compute and token demand pulls in foreign currency for settlement. Every point of dollar strength that results taxes the tradable sector the buildout is supposed to catalyze. The reindustrialization coalition and the deindustrialization mechanism live inside the same system, now running on two commodities instead of one. The US dollar real broad effective exchange rate hit 115 in January 2025 — its highest in roughly forty years.

The hollowing does not fall evenly. The Andurils, Saronics, and Valar Atomics are largely insulated: they sell into the Department of Defense, into dual-use markets, or into domestic demand where price competition with Chinese producers is moot or managed by tariff and subsidy. The currency does not tax them because the buyer is not price-sensitive in the way a global market is. The damage falls on the layer underneath — the specialty steel mills, the foundries, the wire and cable plants, the precision tooling shops, the second-tier electronics. These are exactly the firms that constitute the backbone of a serious reindustrialization. You can build Anduril’s Arsenal-1 with an overvalued currency. You cannot build the supply chain that feeds Arsenal-1 with one. It is impossible for the Department of Defense to subsidize every layer.

There is also a second tension underneath the first. The petrodollar was anchored to a physical commodity. Oil kept flowing regardless of the state of the economy. Demand for oil was structurally inelastic; the modern industrial economy required it, with no substitutes at scale.

The Token Dollar inverts these properties. Tokens exist only at the moment of their consumption and are produced by firms whose valuations rest on the belief that the next model will be a better iteration of the last. They are sold to enterprises whose willingness to pay rests on token consumption leading to productivity gains, and are financed at the margin by allocators whose overweight exposure rests on American firms continuing to dominate the frontier. The bottom layers of the system rest on transactional demand and reserve mandates, while the top layer rests on belief. And it is the top layer that sets the price, and the top layer that flees first when trouble arrives.

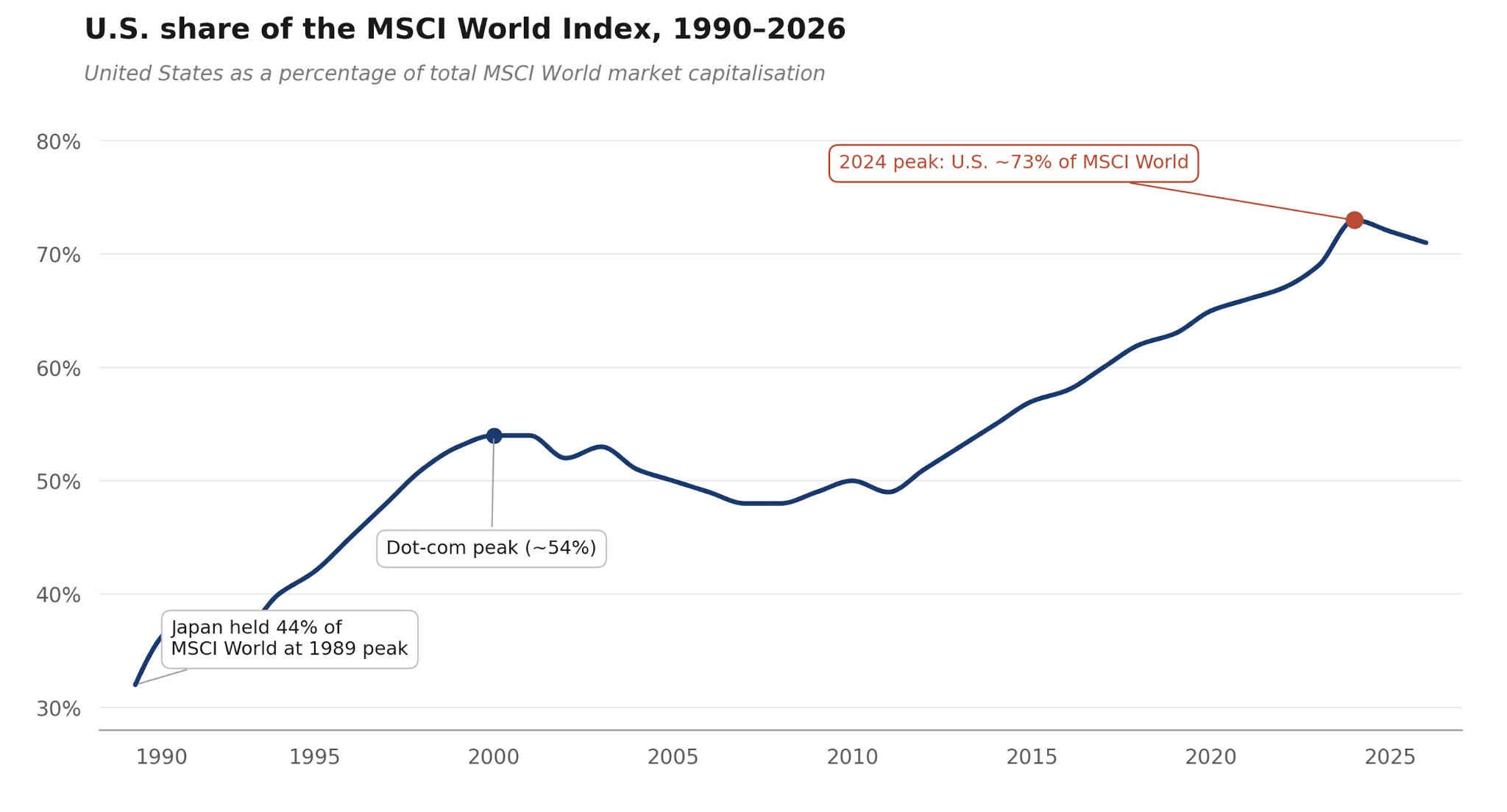

The concentration this implies is hard to overstate. US share of the MSCI World Index reached 73.94% at end-2024, exceeding Japan’s 44% peak in 1989 and the dot-com 54%. One assumption now holds the entire structure together: that the American AI stack continues to command a premium large enough to justify the conversion into dollars in the first place.

That assumption is the load-bearing wall, and unlike oil it is contestable. Oil was geographically scarce; OPEC could be co-opted into dollar pricing because the resource sat under their soil. But on the other hand, compute is reproducible. Anyone with capital, fabs, and power can produce tokens. China already has two of the three at scale, and the third, frontier fabs, is the only thing the US export-control regime is buying time against. DeepSeek and Qwen are already close to frontier capabilities and their open-weight nature means that a European manufacturer or an Indian software firm can run them locally for a fraction of the cost of American frontier intelligence. Advances on the open-weight front that close the capability gap erode the price premium the token dollar fully depends on. The premium still holds today because the US owns the frontier, TSMC and the major labs. But none of those advantages are permanent on a five to ten year outlook. The regime works as long as the premium holds.

To add another dimension, every prior reindustrialization in history was carried out by a country with sovereign control over its currency. The United States is attempting the first exception.

V. No Good Options

The fragility of the Token Dollar shows up first in the response function. Every tool the postwar toolkit depends on stops working in the regime being built.

Consider the Fed in the next downturn. In every prior cycle, the response was the same: cut rates to support the real economy and let the dollar weaken. Recycled foreign surpluses absorbed the issuance automatically. The petrodollar’s holders were captive — central banks holding Treasuries under mandate, oil exporters with no alternative settlement rail, allocators with no benchmark that did not overweight the United States. The bid was structural and the Fed could ease without watching the dollar break.

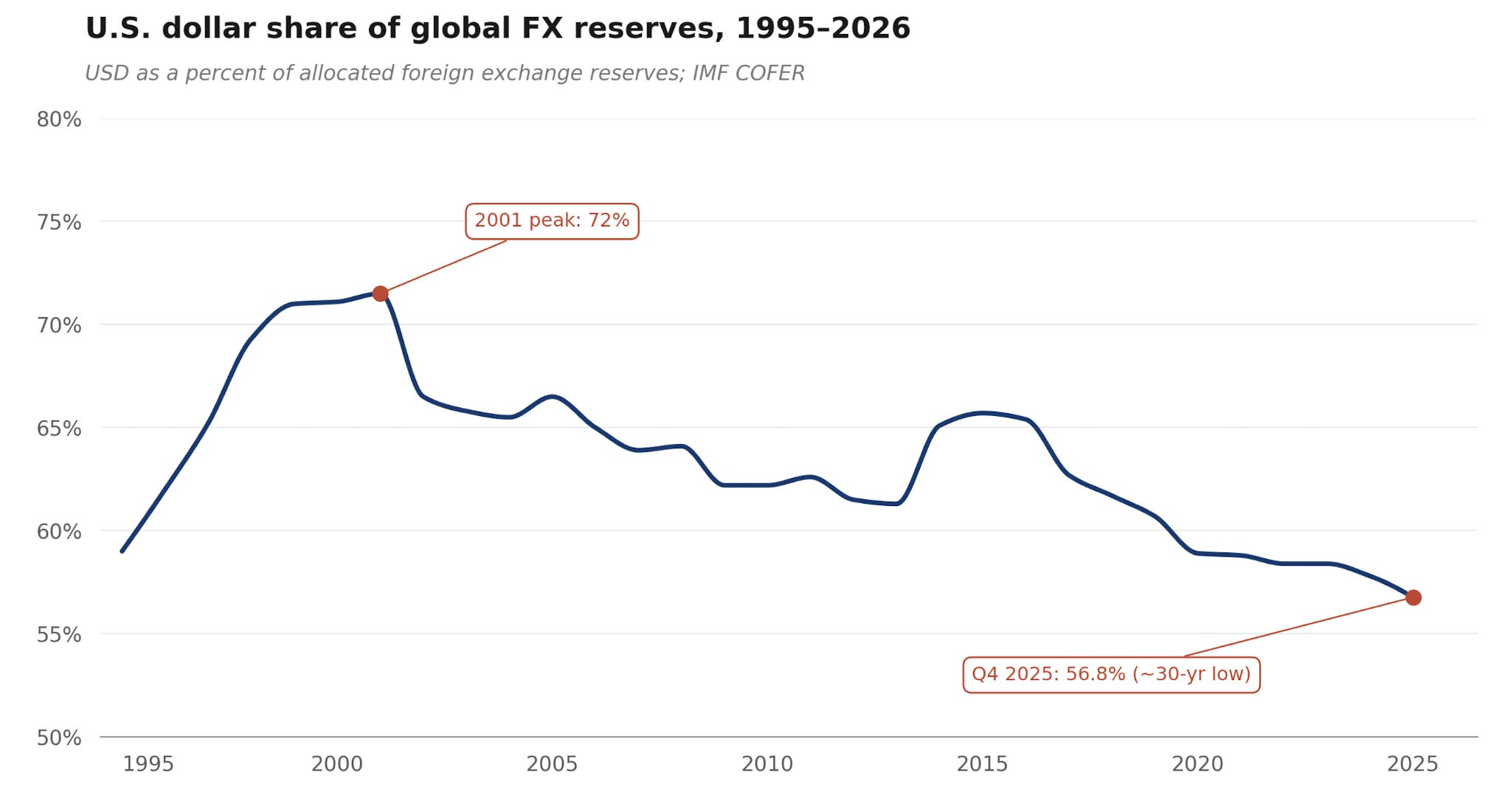

The Token Dollar inverts this dynamic. The marginal foreign holder of American assets today is a private portfolio allocator who is choosing to be there, rebalancing against benchmarks they are free to reweight, with alternatives that are fragmented but growing. The captivity is gone, and what replaces it is choice. And choice, under stress, is what produces capital flight. The USD share of allocated FX reserves has fallen from a 72% peak in 2001 to 56.9% in Q3 2025, a thirty-year low. In every prior cycle, the dollar caught a haven bid even when the Fed cut. Under the Token Dollar regime, that reflex inverts. The marginal holder is no longer reaching for safety. They are reaching for return and they will exit on the way down.

The Fed therefore faces a tradeoff most of its postwar predecessors did not confront. Cut rates to support the real economy and watch the dollar weaken as foreign allocators accelerate their rotation out of AI equities and foreign enterprises delay discretionary compute purchases. Hold rates to defend the dollar and suffocate the AI capex cycle that is propping up the rest of the growth. In the first case, the dollar breaks. In the second, the growth engine breaks. Where the Volcker Fed could choose to break inflation by breaking the labor market, this Fed faces a tradeoff in which both choices break something load-bearing in the regime itself.

Fiscal policy inverts in the same way. In the petrodollar era, deficits widened into a market that was buying. Recycled surpluses absorbed Treasury issuance without a funding crisis for fifty years. In the Token Dollar era, the buyer of last resort is the Fed itself. Countercyclical fiscal response requires monetization and monetization produces dollar weakness. Dollar weakness in turn accelerates the rotation out of dollar assets and weakens the compute settlement flow that depends on foreign enterprises treating dollar-priced compute as a non-discretionary input. The fiscal tool that was supposed to stabilize the downturn becomes a second-order accelerant of the capital flight it was meant to prevent.

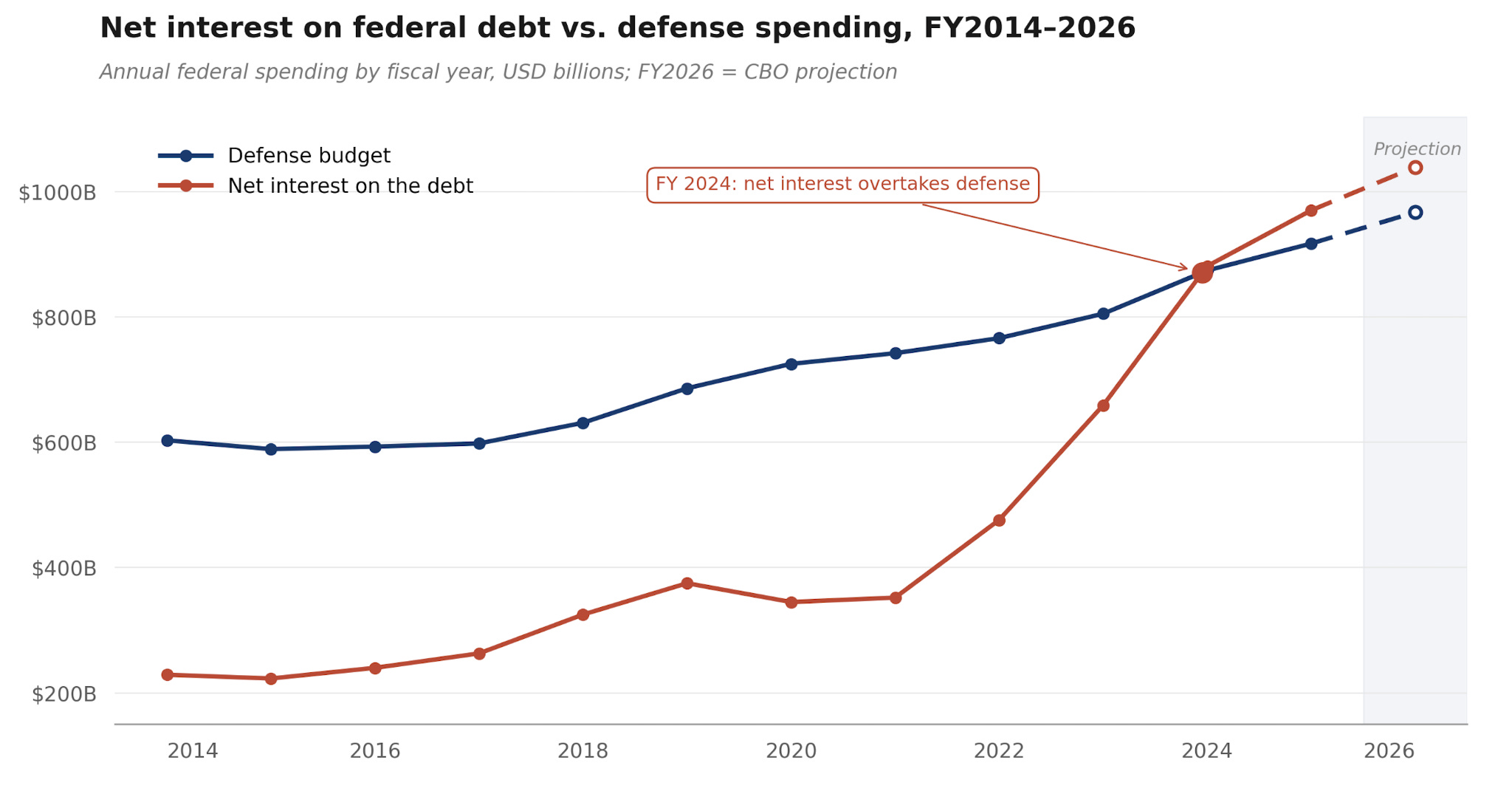

The fiscal arithmetic closes the remaining exits. Net interest on debt overtook defense spending in 2024 and reached $970 billion in 2025, on track to cross $1 trillion in 2026. Federal debt held by the public reached 100% of GDP at year end 2025, and CBO projects 118% by 2035. Inflation cannot clear the debt without destroying the dollar. Rate cuts cannot clear it without unwinding the dollar. Growth cannot clear it because growth requires the tradable sector the currency is currently taxing.

The instruments that absorbed every prior shock — Fed easing, fiscal expansion, the captive bid for Treasuries — were built for a system whose holders could not leave. The Token Dollar’s holders can. And if they do, then the Fed will be choosing between two breakages, neither of which it can prevent.

VI. Hard Choices

If the previous section is the diagnosis, the question of what gets done forces a tight hand of options, none of them clean.

Subsidize the differential. Pay the cost gap between US and foreign production through industrial policy at scale. CHIPS, IRA, DPA invocations, and emerging compute industrial policy are good first attempts. But to really make the math work, they likely need to grow by an order of magnitude. The fiscal cost is large, but for a country whose debt is the world’s reserve asset, financing is the easiest part of the equation. This is more a question of our political appetite and how much financial repression we can shift abroad.

The Miran Plan. Stephen Miran’s User’s Guide to Restructuring the Global Trading System, published in late 2024, has become the closest thing to a doctrine for the second Trump administration’s economic policy. Its proposals attempt to thread the needle of preserving reserve currency status while weakening the dollar for tradeables. Tools such as aggressive tariffs, leveraging US security guarantees to pressure allies into accepting dollar weakness, converting allied Treasury holdings into century bonds, and charging user fees on foreign Treasury holdings, could help achieve this seemingly impossible goal. The premise is that the US can selectively bend the regime because of its leverage over trading partners.

Sovereign vendor finance. The United States lends dollars to foreign sovereigns who use the proceeds to purchase US-produced AI services and infrastructure. This is the structure being assembled in major deals with the UAE, Saudi Arabia, and various Asian partners. This has stark similarities to the Marshall Plan. If institutionalized and carried out at scale, it could become the main mechanism by which token dollar demand is created and satisfied without forcing a domestic cost reckoning.

National capitalism. Russell Napier has argued for several years that we are exiting the era of central-bank-mediated globalization and entering a new era of state-directed capital allocation. He terms this “national capitalism.” Governments compel banks to lend into strategic sectors at administered rates. Inflation runs hotter than nominal rates, turning real return on savings negative. A quiet tax on savers that simultaneously erodes the real value of government debt and channels credit toward whichever sectors the state has chosen to favor. Napier argues that it is already emerging in various forms: “buy american” provisions, the politicization of bank lending, and capital controls in surprising places. This outcome is not market-based at all. The state would simply force capital into the buildout regardless of price signals and accept the inflation.

Productivity escape velocity. The most optimistic resolution and the one preached by technologists: AI productivity gains bend the cost curve fast enough that the strong dollar ceases to matter. AI deflationary forces would outweigh the strength of the currency. Hence, a flywheel is unlocked: the buildout produces the productivity that makes further buildout economically viable. The question is timing. The financing must hold long enough for the productivity gains to arrive at scale.

Regime change. The final option is the one no policymaker advocates for and history occasionally imposes: the dollar simply ceases to be uniquely the world’s reserve currency. Erosion can happen along three channels: i) The American AI premium fails as China reaches frontier parity with open-weight models, ii) foreign holders conclude that dollar assets carry political risk on top of market risk, because Napier-style capital controls or Miran Plan’s user fees signal that the holdings really are not neutral property, and iii) Triffin’s old paradox closes, similar to the sterling between 1914 and 1956. The token-dollar thesis fails not because tokens aren’t valuable but because the dollar is displaced. The world becomes monetarily multipolar and the exorbitant privilege ends. US tradeables become competitive again, but the cost of capital rises and the financialized superstructure of the past forty years contracts. The ouroboros eats its own tail so to speak.

What actually gets done will be some combination between the options above. None is sufficient alone and all of them are racing the same clock. Policy will have to build the token dollar while reversing the deficit dynamic the petrodollar entrenched without surrendering the reserve currency status.

The Token Dollar thesis is the most ambitious bet on dollar dominance since Kissinger’s 1974 trip to Riyadh. Kissinger’s bargain worked because oil could be pumped without US industrialization. Tokens cannot. To anchor the dollar in compute, the United States must do what the dollar regime has never permitted any reserve issuer to do: become the world’s factory while remaining the world’s banker. None of the available choices makes this easy. Most of them require shedding parts of the regime that the policy class has been accustomed to treating as permanent. The hardest part of the conversation now beginning may be admitting how much of the old order must go to make the new one work.

Musical Coda:

Bach – St Matthew Passion BWV 244 (Youtube)

| A guest post by

|

This is great. Really good stuff.

incredibly insightful piece!!